IRS Form 1310: How to Fill it Right

It is essential for tax payers to know how to fill in IRS Form 1310. Find the instructions for IRS Form 1310 in this article.

100% Secure |

100% Secure | Home

>

Other IRS Forms

> IRS Form 1310: How to Fill it Right

Home

>

Other IRS Forms

> IRS Form 1310: How to Fill it Right

IRS Form 1310 allows an eligible person to claim a refund on behalf of the deceased when a taxpayer has passed away, and a federal tax refund is due. Understanding when Form 1310 is required, who qualifies to file it, and how to complete and submit it correctly is important to avoid delays or rejection by the IRS.

File Taxes Faster with PDFelement

Scan receipts and paper forms into searchable PDFs

Compress large PDFs for easy storing and sharing

Securely save and back up tax records as PDFs

Organize tax files by year and category

Merge related tax forms, statements, and receipts into one file to reduce clutter

Download IRS Form 1310 in PDF - Printable, Fillable

What Is Tax Form 1310

Form 1310, officially titled Statement of Person Claiming Refund Due a Deceased Taxpayer, is used to request a tax refund that was owed to someone who has passed away. The IRS requires this form to ensure that the refund is paid to the correct individual and that the claimant has the legal authority to receive it.

Form 1310 is generally required when a refund is due on a deceased taxpayer’s final federal income tax return, and the person claiming the refund is not a surviving spouse filing a joint return, or the claimant is not a court-appointed personal representative already recognized by the IRS.

If a surviving spouse files a joint return with the deceased, Form 1310 is usually not required. In other cases, the IRS uses Form 1310 to verify the relationship and authority of the person claiming the refund.

Tax Form 1310 Instruction for 2026

How to Fill out Tax Form 1310

Before completing IRS Form 1310, it is important to gather all required information and documents.

You should prepare the following:

- A copy of the deceased taxpayer’s death certificate or other official proof of death

- The deceased taxpayer’s final federal income tax return (Form 1040 or 1040-SR)

- Supporting income documents, such as Forms W-2, 1099, or other tax statements

- Your own personal information, including your Social Security number and mailing address

- Court appointment documents, if you are a court-appointed personal representative

Once you have gathered the necessary information, you can complete Form 1310 by following each section carefully.

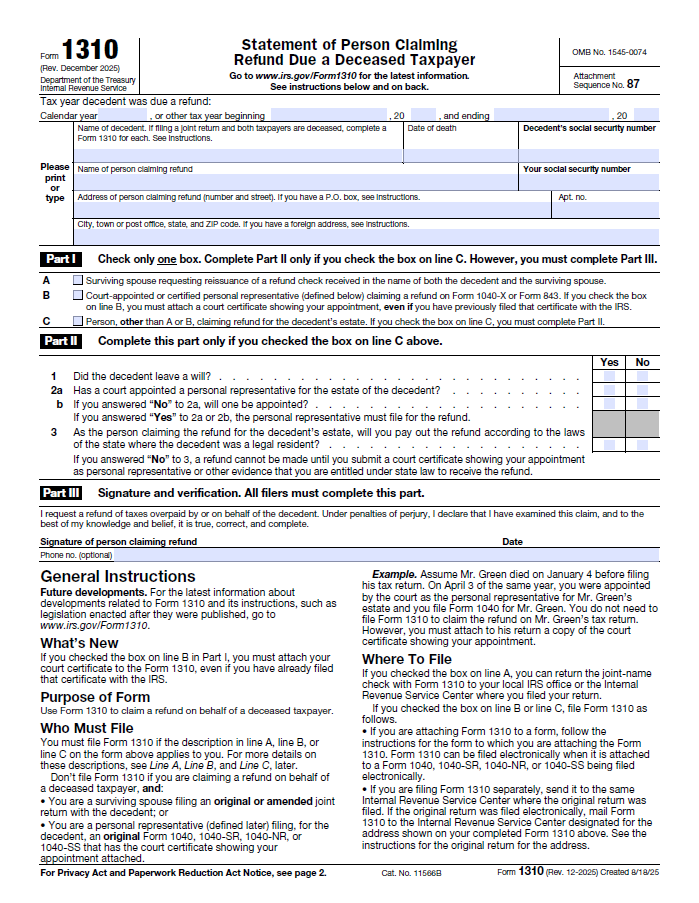

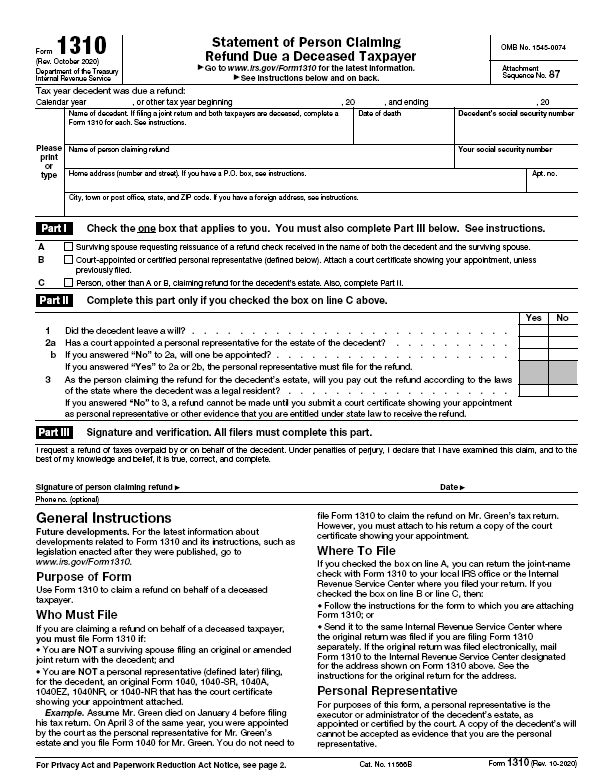

Top Section At the top of the form, enter the tax year for which the refund is being claimed, along with the deceased taxpayer's name, Social Security number, and date of death. You must also provide your own name, address, and Social Security number as the person claiming the refund.

Part 1 This part determines your eligibility to claim the refund.

- Line A is checked if you received a refund check made payable to both you and your deceased spouse. In this case, the original check must be returned to the IRS marked “VOID,” along with Form 1310 requesting that the refund be reissued in your name only.

- Line B is checked if you are the court-appointed or certified personal representative of the deceased taxpayer’s estate. If you are filing an amended return or refund claim, attach a copy of the court certificate showing your appointment. If the certificate was previously sent to the IRS, write “Certificate Previously Filed” on the form.

- Line C is used if neither Line A nor Line B applies. In this situation, you must submit proof of death, such as a death certificate or official notice from a government agency.

Part 2 This part asks questions about the deceased taxpayer’s estate. You will indicate whether the decedent had a will and whether a court has appointed, or will appoint, a personal representative. You must also state whether the refund will be distributed according to state law. If not, the IRS may require additional documentation proving your legal authority before issuing the refund.

Part 3 This part is the certification section. Here, you sign and date the form to confirm that you are entitled to the refund and that all information provided is accurate. You may also include a daytime phone number in case the IRS needs to contact you.

After completing Form 1310, attach it to the deceased taxpayer’s final income tax return and submit both together according to IRS filing instructions.

If you are handling tax form electronically, Wondershare PDFelement - PDF Editor Wondershare PDFelement Wondershare PDFelement is your great PDF helper for you to fill PDF form, print PDF, edit PDF, sign PDF, compress and convert PDF. It is quick, straightforward, and easy and can be done by beginner-level user.

G2 Rating: 4.5/5 |

G2 Rating: 4.5/5 | 100% Secure

100% Secure

Where to Mail Form 1310

Form 1310 is not filed on its own. It is submitted together with the deceased taxpayer's final federal income tax return.

If you are filing a paper return, mail Form 1310 and the tax return to the IRS address listed in the instructions for Form 1040 or Form 1040-SR, based on the taxpayer’s state of residence. IRS Mailing Address: Where to Mail IRS Payments

For additional help, visit the instructions of form 1310 on IRS webstie for more details.

Does a Personal Representative Need to File Form 1310

A personal representative is a person legally authorized to manage the deceased taxpayer’s estate. This authority usually comes from a court appointment, such as an executor named in a will, or an administrator appointed by a probate court.

If you are a court-appointed personal representative, you generally do not need to file Form 1310, provided you attach a copy of the court appointment documents to the tax return. The IRS uses those documents to confirm your authority.

Tips and Warnings for IRS Form 1310

- Tips and Warning for IRS Form 1310 The information provided in this form will be used to determine your eligibility to internal revenue code of section 6012 to claim the refund due to the decedent. You do not have to provide the information asked for on a form until the form shows a valid Office of Management and Budget (OMB) control number.

- The instructions provided in these forms must be read again and again until it is clear, these forms have many elements which are difficult to grasp. You will surely make errors if you submit such forms in a hurry, never keep such work pending for the last day. Also try to use a PDF form filer like PDFelement to remain focused for completing it at once.

- The information provided will be reviewed by the Internal Revenue Service so, make sure the data you are providing are valid and backed by valid documents. If any tax related form submitted is found with false or counterfeit information, the government will take essential steps against that person.

- You must have the proof of death certificate and the formal notification of the next kin of the decedent's death. You do not have to attach the proof of death to form 1310 but you must keep a copy of it and provide if necessary.

Free Download or Buy PDFelement right now!

Free Download or Buy PDFelement right now!

Try for Free right now!

Try for Free right now!

Audrey Goodwin

chief Editor